Introduction

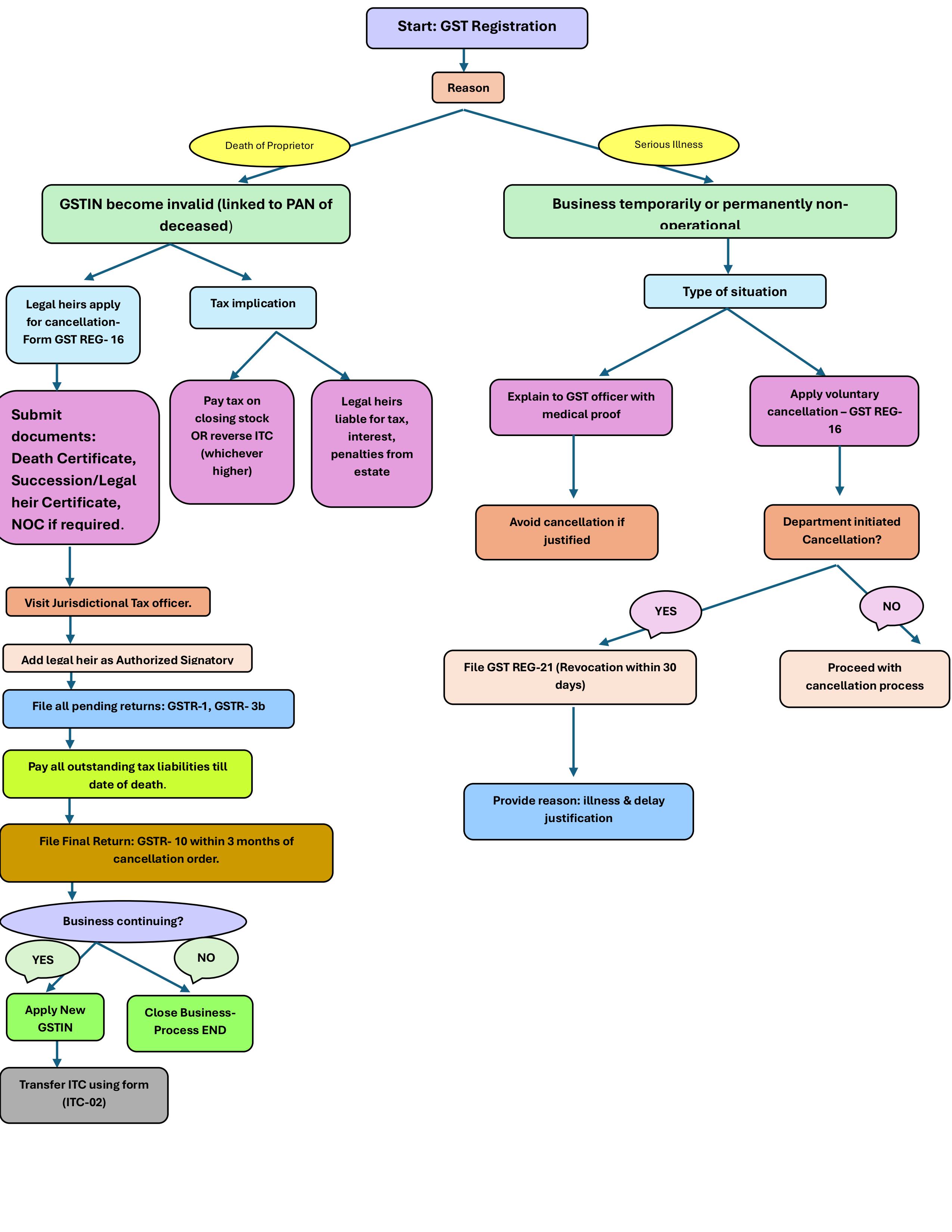

When a sole proprietor dies or is unable to continue due to serious illness, the GST registration must be formally closed since the GSTIN is linked to the individual’s PAN. In case of death, the legal heir first gets added as an authorized signatory through the jurisdictional officer, files all pending returns (GSTR-1 and GSTR-3B) and clears dues, and then applies for cancellation using Form GST REG-16 along with documents like the death certificate and legal heir proof. If the business is to be continued, a new GSTIN is required and input tax credit can be transferred through Form GST ITC-02. In cases of serious illness, temporary non-operation can be justified to avoid cancellation, but for long-term closure the same cancellation process applies; if registration is cancelled by the department due to non-filing, it can be revoked within 30 days using Form GST REG-21.

Conclusion.

Finally, Form GSTR-10 (Final Return) must be filed within 3 months of cancellation, declaring details of closing stock (inputs, semi-finished and finished goods), capital goods, and computing tax payable on such stock or reversal of ITC, whichever is higher, along with any pending liabilities to ensure full settlement. In recent GST cancellation cases, the portal has also been asking for or providing an option to upload a Chartered Accountant or Cost Accountant certificate related to closing stock details as supporting documentation for verification purposes.